Provide customers with a simple to use, mobile-focused platform for making and arranging payments which take their personal circumstances into account, while also increasing repayments and automating the collections process.

Data reveals that the key to sustainable and ethical debt collection is through flexible payment options and a mobile-first communication and collections strategy.

Household debt has increased by 7.3% over the last five years, while wages have grown just 0.7%, leading the Office for Budget Responsibility (OBR) to predict that unsecured household debt will reach 47% of income in 2021 (source).

Additionally, the poorest 10% of UK households have debt three times the value of their assets (source). Companies chasing payment not only have to contend with the debtor’s ability to pay, but also compete with other companies making demands.

With this in mind, it’s small wonder that the UK debt purchase and debt collection industry has grown by 30% in just five years (source) – and equally, that robust rules around the fair treatment of customers are enforced by the FCA.

The challenge is clear: make sure you get paid without making the debtor’s situation worse.

How to recover more debt fairly

Historically, a standardised ‘PAY NOW’ approach has been used by many businesses, which doesn’t offer the flexibility required by customers to make payments on their terms.

Coupled with this, traditional forms of payment such as reading card details aloud to an agent, or completing a paper-based form, are much less convenient for customers as calls can come at inopportune times, and letter-based reminders often require details to be physically mailed back.

There are also direct drawbacks for the businesses themselves still using traditional payment channels. Low engagement results in low collection rates, and the cost of using traditional channels like post and manual calling means that the value of the debt being chased is often less than the cost to chase it, resulting in debt being written off.

Mobile Collections provides an alternative approach; a convenient, self-serve platform which offers convenient payment options to adhere to the FCA’s guidelines.

The platform, which is designed to be accessed on a mobile device, builds trust by matching the branding of the company requesting payment. Customers receive a personalised link via text or email, allowing them to choose when to respond. Customers can make a payment, set up a repayment plan, make a promise to pay or choose to speak with an agent through their preferred channel if they need to chat.

Mobile Collections also allow you to fully automate your whole collection strategy by sending out reminders and notifications when payments are due, or when plans are not kept up to date.

All this allows your customers to self-serve, which in turn increases your collection rates and significantly lowers your cost to serve.

Do Mobile Collections work?![]()

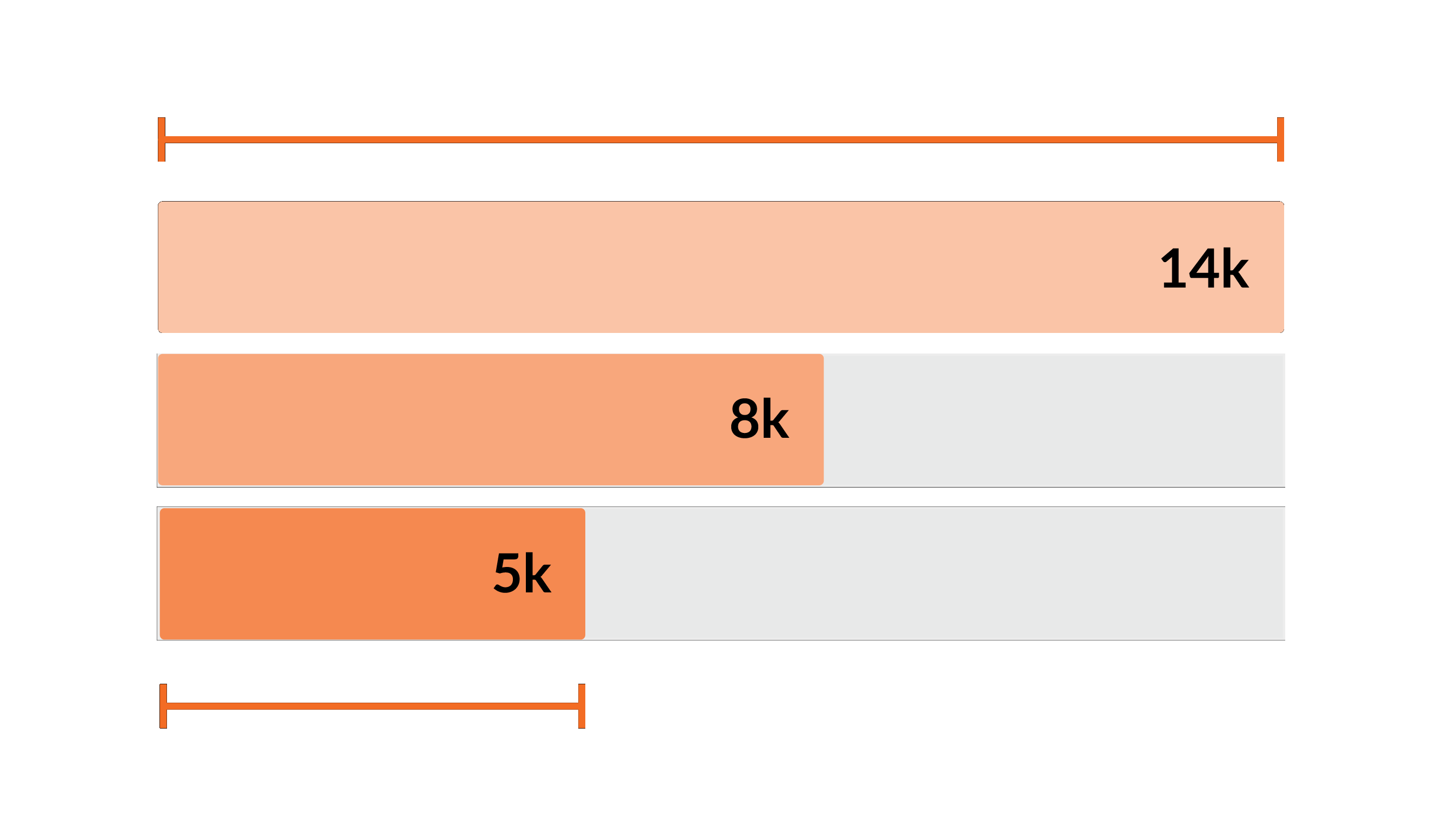

We conducted a study of 14,000 customers who had been sent a link to their own Mobile Collection. 8,000 of those customers clicked on the link and opened the Mobile Collection environment, and just over 5,000 went on to make a payment – that’s 38.2% compared to an average successful collection rate of 20% (source).

We’ve worked with a wide variety of different business types, from debt collection agencies to in-house collection teams, who were looking for more engaging ways to collect payments and arrange payment plans with their customers, in ways that not only help collect more debt, but also lower their cost to serve.

To find out how we could do the same for your business with a Mobile Collections solution, please get in contact with our team today by calling 0345 356 5758 or emailing [email protected]

Esendex

The team at Esendex comprises tech experts and experienced marketers who thrive on sharing their know-how, to support prospects and customers to identify the right mobile messaging solutions for their business.